Selling a House During

Financial Hardship in Florida.

We Can Help.

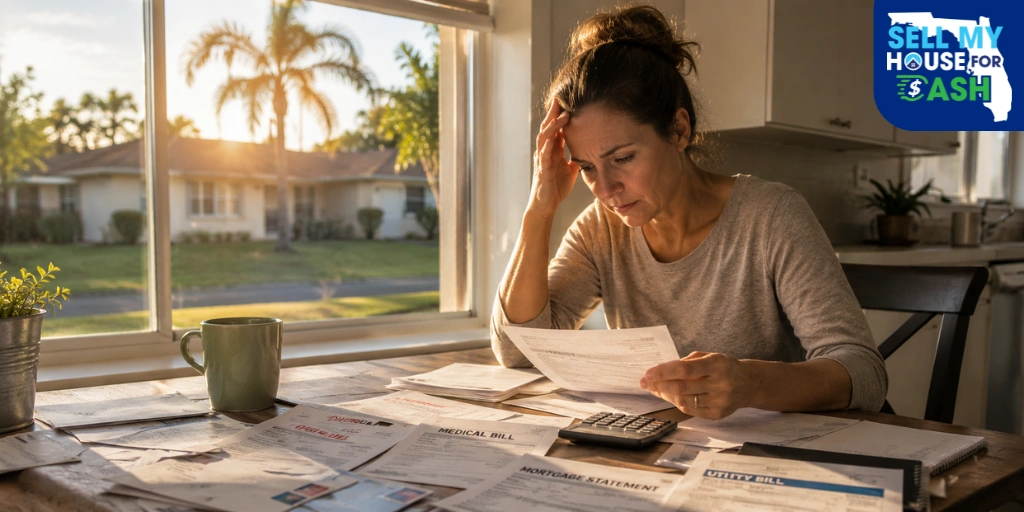

Job loss, medical bills, divorce, business failure. Financial hardship takes many forms. Whatever brought you here, there is no judgment. Our job is to help you understand your options and get from where you are today to where you need to be.

Financial hardship is not a character flaw. It is a circumstance. Job loss, a medical crisis, a divorce, a business that did not survive. These are things that happen to good people who made reasonable decisions. If you are here, you are looking for a way forward. That is exactly what we are here to help you find.

A home is the largest financial asset most people own. Deciding what to do with it during a difficult period deserves careful thought, honest advice, and no pressure. We will walk you through every option available to you. Not just the one that benefits us. If selling to us makes sense, we will show you the math. If another path puts more money in your pocket or keeps you in the home, we will tell you that too.

Financial hardship looks different for every homeowner. Here are the five most common situations.

Whatever brought you here, you are not alone. These are the situations we hear most often from Florida homeowners who call us.

Job loss or significant income reduction

The income that made the mortgage manageable is gone or reduced. Every month the gap between what you earn and what you owe grows wider. You may have used savings to cover payments for a while. That runway is running out. The mortgage that felt comfortable two years ago is now unsustainable.

Medical bills or a health crisis

A serious illness, a hospitalization, or an ongoing condition has generated bills that savings and insurance could not fully cover. The financial impact compounds. Reduced ability to work, increased costs, depleted reserves. The home may be the only asset large enough to provide real relief.

Divorce or separation

What two incomes covered comfortably is now impossible on one. The house may be jointly owned with a complicated split, or one party may be on the mortgage and unable to qualify for the payment alone. The property is often the most complex and most valuable asset to resolve in a separation.

Two additional situations we see regularly: business failure or investment loss. Cash flow that supported the mortgage has collapsed, and the home is now carrying more weight than it was designed to — and death of a co-borrower or supporting spouse. The obligation remains but the income or support that made it manageable is gone. Every one of these situations is treatable. None of them is hopeless. The path forward starts with understanding what your options actually are. For free independent housing counseling from a HUD-approved advisor, see: HUD housing counseling services.

Not sure which situation applies to you? Call us. You do not need to have it all figured out before you reach out. Tell us what is happening and we will help you understand what options are available. One conversation, no cost, no commitment.

If divorce is the primary reason you need to sell, see our dedicated guide: Selling a House During Divorce in Florida. If foreclosure proceedings have already started, see: How to Stop Foreclosure in Florida.

We will only buy your property if it puts you in a better position than you are right now.

This is the most important thing we can tell you.

We are on your side. Advisor first, buyer second.

If we believe that selling your house is not in your best interest, we will tell you. And we will point you toward a better path if one exists. Sometimes the right answer is listing the property with an agent and waiting for a retail buyer. Sometimes it is a loan modification that keeps you in the home. Sometimes it is a short sale that avoids foreclosure on your credit. Sometimes it is a cash sale that closes in three weeks and gives you the equity to start over. Our job is to understand what you are going through and help you get from where you are today to where you need to be. We will never make you an offer simply because you are in a difficult position and might accept it. We make an offer because the math works for you and the outcome improves your situation.

Your home is your biggest asset. We treat it that way.

A home is the largest financial asset most people own. Selling it is one of the most significant financial decisions a person can make. We walk you through the full closing math on the first call. What you owe, what you net, what you walk away with. Make a fully informed decision before you commit to anything. If another option puts more money in your pocket, we will tell you and point you there. A good outcome for you is what creates our reputation. That matters to us.

The numbers above are illustrative. Every situation is different. What does not change is the process. We show you every line before you sign anything. For free independent advice from a housing counselor not affiliated with us, see: HUD-approved housing counseling.

Not sure if selling is even the right move? Call us before you decide anything. We will walk through all your options. Loan modification, listing with an agent, short sale, cash sale. Give you an honest assessment of which one makes the most sense for your specific situation. No commitment required.

Before you decide anything, understand all your options.

Most people in financial hardship focus on the most obvious option. Sell or do not sell. The full picture is broader than that. Here is every path available to Florida homeowners in financial difficulty.

Loan modification

Your lender restructures the terms of your mortgage. This could mean reducing the interest rate, extending the loan term, or temporarily reducing the payment. This is the best option if you want to stay in the home and your lender is willing to work with you. It takes time and requires documentation of your hardship. A HUD-approved housing counselor can help you navigate this process at no cost to you.

Forbearance

Your lender temporarily pauses or reduces your payments for a defined period. This buys time but does not erase the debt. The missed payments are typically added to the end of the loan or repaid over time. Forbearance is useful when the hardship is temporary and you expect your income to recover.

Listing with an agent

If you have time, equity, and a property in reasonable condition, listing with an agent may yield the highest sale price. The tradeoff is time. Typically 90 to 120 days from listing to closing, and 5 to 6 percent in commissions plus closing expenses. If foreclosure proceedings have not started and you have several months of runway, this may be the right path. We will tell you honestly if we think it is.

Short sale

If the total amount owed exceeds the property value, a short sale allows the lender to accept less than the full mortgage balance in order to avoid foreclosure. Short sales require lender approval and take longer than standard sales but avoid the severe credit impact of foreclosure. A real estate attorney is strongly recommended for short sale situations.

Cash sale

The fastest and most certain path. We close in 3 to 4 weeks, pay off all liens and arrears at closing, and wire the remaining equity to you. No commissions, no fees, no repairs required. The best option when time is short, the property has condition issues, or foreclosure is imminent. We will only recommend this path if the net proceeds put you in a genuinely better position.

For a full breakdown of how the cash offer option compares to a traditional listing, read: Pros and Cons of a Cash Offer on a House. To understand net proceeds after fees and costs: How much do you lose selling a house as-is?

Three ways Florida homeowners in financial hardship sell their property

If selling is the right path for your situation, here is an honest look at the three options.

Not sure which option fits your situation? Call us. We will walk through all three honestly and tell you which one makes the most financial sense for where you are right now. Including options that do not involve us.

Why acting sooner almost always produces a better outcome

This is not pressure. It is math. When financial hardship involves missed mortgage payments, every month of delay adds late fees, penalties, and accrued interest to what you owe. The equity you have today is worth more than the equity you will have in three months after another quarter of missed payments and fees. Foreclosure proceedings, once filed, reduce your options significantly. Some lenders become unwilling to negotiate. Some buyers walk away from properties in active foreclosure. The credit impact begins regardless of whether the property eventually sells.

Acting while options are still open is almost always better than waiting until only one option remains. If you have equity today, a cash sale this month may put $80,000 in your pocket. The same property in foreclosure six months from now may yield nothing after legal fees and penalties consume what was left. One conversation with us costs nothing and clarifies everything. Even if you decide not to sell, you will leave that call knowing more than you knew before.

Already missed payments or received a foreclosure notice? Call us today. The sooner we talk, the more options are still available. See our full guide on stopping foreclosure in Florida: How to Stop Foreclosure in Florida.

What if the property has liens, arrears, or other complications?

Financial hardship rarely comes alone. Properties in financial distress often also have unpaid property taxes, HOA liens, code violation fines, or judgment liens recorded against the title. None of these prevents a cash sale.

Every lien, every arrearage, every outstanding balance is paid from the sale proceeds at closing. The title company coordinates the payoffs. You do not need to negotiate with the IRS, the HOA, or the code enforcement office before accepting an offer. Whatever equity remains after all balances are cleared comes to you. We show you that exact number before you commit to anything.

If the property has condition issues on top of the financial complications. Deferred maintenance, vacancy damage, or repairs that never got done because the money was not there. Those are factored into the offer upfront. There are no surprises after the fact. The offer we make accounts for everything we can see and everything you tell us.

Have liens, missed taxes, or HOA arrears on the property? Call us before doing anything else. We will confirm what is owed, factor it into the offer, and show you exactly what you net. You never pay these out of pocket before the sale. They are resolved at closing from the proceeds. See also: Selling a House with a Lien in Florida.

Five mistakes Florida homeowners make during financial hardship

These are the mistakes that cost hardship sellers the most money and close off the most options.

Waiting too long while equity erodes and options close

Hoping the situation improves, avoiding the calls, putting off the decision. All of these feel like they preserve options when in reality they consume them. Every month of missed payments adds to what you owe and reduces what you net. Every month closer to foreclosure narrows the buyer field. The sellers who call us earliest almost always walk away with the most.

Taking the first offer without understanding all options

Urgency and desperation can make a bad offer feel like the only offer. Before accepting any cash offer, including ours, understand what listing with an agent would realistically yield, what a loan modification might accomplish, and what your actual net would be across all paths. We will help you run that comparison on the first call. See: How much do you lose selling a house as-is? If you are exploring the no-agent path: How to Sell a House Without a Realtor in Florida.

Not disclosing the full financial picture to the buyer

Florida requires disclosure of known encumbrances, liens, missed payments, and material defects. A buyer who discovers undisclosed financial complications after the offer is accepted can reduce the offer, delay the closing, or withdraw entirely. Tell us everything upfront. Liens, arrears, missed payments, condition issues. A cash buyer who knows the full picture has already priced it in and will not come back with a lower number after the fact.

Letting shame prevent action until foreclosure is filed

Financial hardship carries a stigma it does not deserve. Many sellers wait far too long before reaching out because they feel embarrassed about their situation. By the time they call, foreclosure has been filed, the credit damage is done, and the options that were available six months earlier are no longer on the table. There is no judgment here. The sooner you call, the more we can do.

Choosing a buyer who exploits urgency rather than respects it

Not every cash buyer operates the way we do. Some make attractive initial offers and reduce them after inspection knowing that a seller in hardship has limited ability to push back. When we make an offer we have already done the work. Our partner investors verify the property during the inspection period. If the condition matches what you described, the price holds. If something significant was not disclosed, we explain exactly what it is and why. Nothing is final until you say it is. Walk away at any point. No pressure, no hard feelings. Read what our sellers say: verified Google reviews.

Why Florida homeowners in financial hardship trust Sell My House For Cash Florida

Financial hardship requires a buyer who earns trust before asking for a commitment. Here is how we approach every hardship seller conversation.

We are honest. Even when the answer is not us.

If listing with an agent or pursuing a loan modification puts more money in your pocket or keeps you in your home, we will tell you that. Our reputation is built on sellers who got the right outcome — not just sellers who sold to us. Learn more about who we are: About Us.

Offer based on value. Not on how badly you need to sell.

We use the same ARV formula for every seller regardless of their circumstances. Your urgency does not change the math. The offer reflects the property value and real repair or lien costs. Not your financial situation. That is the only fair way to do this.

Close in 3 to 4 weeks. Before more equity erodes.

Every month of delay in a hardship situation has a cost — late fees, penalties, accruing interest, and foreclosure risk. We close in 3 to 4 weeks. That stops the bleeding. See how the process works: How We Buy Houses.

Full closing math on the first call. Nothing hidden.

We walk you through every line of the offer calculation before you commit to anything. Mortgage payoff, lien payoffs, your net proceeds. If our partner investors identify a major undisclosed issue during the inspection period, we explain exactly what it is and why. You are never obligated to accept any revision.

"Juan was honest with me from the very first call. He explained everything clearly, never pressured me, and followed through on exactly what he promised. Selling to him was the right decision and I am glad I made the call when I did."

One conversation.

No commitment. Just clarity.

Tell us what is happening. We will walk through your options honestly. If a cash sale makes sense, we will show you the math. If another path is better for your situation, we will tell you that too. Either way you will leave the call knowing more than you knew before.

Get a free offer. Or just talk through your options. No pressure.

"*" indicates required fields

No obligation. No pressure. No spam. Your information is never shared.

Prefer to talk? Call us at 561-786-7720